|

|

|

|

|

|

OCTOBER 4, 2020

This newsletter is a weekly in-depth analysis of tech and innovation in Africa that will serve as a post-pandemic guide. Subscribe here to get it directly in your inbox every Sunday at 3 pm WAT.

|

|

|

|

|

|

|

|

|

By now, you know how moot the fintech vs banks debate is, especially in the African context. You probably roll your eyes at any of that kind of talk, right? Right!

A Google search will tell you all you need to know; how these fintech companies need banks to survive, and banks in turn act like they need them. And how most importantly this collaborative

ecosystem exists all around the world.

But regardless, on the other hand, the bank vs fintech conversation is real. Maybe not from a debate perspective, but something is happening in Nigeria’s banking industry; the challengers are about to be challenged.

Before we start this conversation, two things to note:

- There are more links than usual in today’s edition; read them all.

- If you are not subscribed yet (I wonder why not), please do so here and catch up on older editions of The Next Wave.

Now, let’s talk Nigerian banks and their younger cousins; fintech startups.

|

|

|

|

|

|

|

A sibling rivalry, kinda.

In an interview with CNBC, Monzo CEO Tom Blomfield raised alarm on how banks are trying to kill fintech innovations by simplistic approaches:

“Banks are set up to prevent change basically,” he said. “A lot of the systems inside the bank — particularly risk and compliance functions — are there to stop things changing. Because if things change it creates risk. And so they’re like these antibodies that go around hunting out change and trying to kill it.”

Blomfields’s concerns are valid, Monzo is in a jungle that I do not envy.

But the collaborative infrastructure in Nigeria is strong: Fintechs need banks for veracity, and banks need them to figure out this millennial market and new infrastructure.

Q4 2015 was the first time I heard the banks vs fintech debate. It was on the steps of CcHub in Lagos, and a meetup had just been rounded up, or was it a pitch now, I can’t remember. Anyway, a group of people were discussing, or more appropriately heatedly arguing, for and against banks killing fintechs.

PayStack was officially a few months into operations at the time, and fintech was starting to gain popularity in Nigeria.

Eavesdropping on the conversation, a couple of thoughts crossed my mind at the time:

- Nigeria’s oldest bank, First Bank of Nigeria was formed in 1894; 126 years ago. This invariable means they have customer data and insight dating back over a century.

- And by extension, are not interested in this fintech hustle, or most likely, data has shown them that it is all a small fry. (Or so it seemed to me at the time).

Regardless of all these, most banks made half-hearted, non-committal plays at fintech that were most likely to show their customers how hip they were.

Five years down the line and it seems all that is about to change, or actively changing; fintech startups are starting to look like serious

contenders.

|

|

|

|

|

In the year ended 2019, according to COO Odunayo Eweniyi, 1 million users saved $80 million. In contrast, First Bank Holdings; the parent company of First Bank Nigeria PLC reportedly did $1.6 billion in revenue for that same period in 2019. These two figures look very mismatched and laughable, but when context is applied; years of existence, current number of customers, etc, those laughs disappear.

[READ:Odunayo Eweniyi: How we built PiggyVest through multiple trials]

Regardless, it is still a mismatched fight of giants. During the pandemic, payday lending apps were going through the pandemic blues.

[READ:Coronavirus Weekly Update: Lending blues]

Meanwhile, Access Bank just came out of a year of unimaginable lending to its customers. According to Nairametrics:

“[it] (Access Bank) claims its Quick Loan Scheme or Payday Loan (as the bank calls it) disburses about ₦200 million daily to 4,600 customers and the bank is eager to double that number to ₦400 million and 20,000 customers by end of the year.”

If you do not see the

juggernauts that fintech players are in the field with, then you should look again.

Regardless of all these, there is a tectonic shift in Nigeria’s fintech space and it’s no more the fintech scrapings from ‘15. Banks have always collaborated with fintech startups, and most of the fintech startups would not exist without banks anyway.

[READ:Nigerian banks want fintech collaborations, but for specific and unique needs]

But beyond a non-committal relationship, that aforementioned 100+ years data is screaming at Nigerian banks to ‘pay attention’ to these startups and see competition, and they seem to be doing just that.

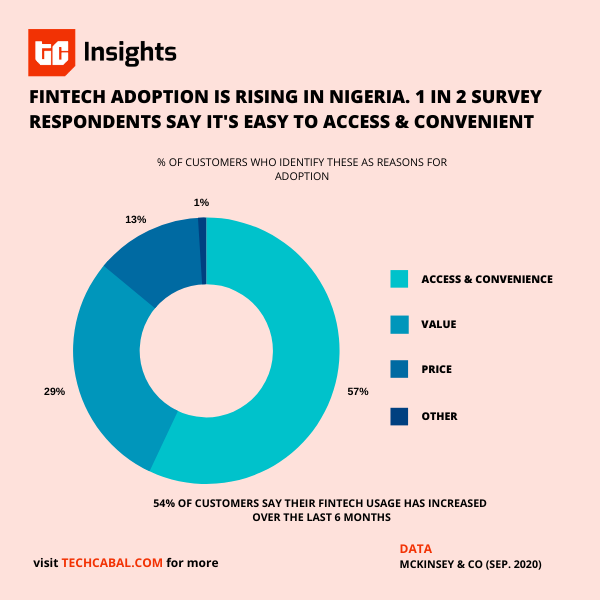

Fintech revenues in Nigeria are projected to grow from $153.1 million in 2017 to $543.3 million by 2022; the potential is mouthwatering.

The holding frenzy

I have a standing (not so funny) joke; Nigerian banks do everything else, except actual banking; fashion fairs, ecommerce, talent discovery, everything. This joke is only funny to my non-Nigerian friends.

In June 2019, I asked a few bank insiders why this is so: short answer? FOMO. For a longer answer, read this article.

[READ: Seemingly driven by fear, Nigerian banks have become everyone’s competition]

A new data-driven FOMO is seeing these banks restructure into holding companies. The frenzy started with GT Bank, and Sterling Bank immediately followed suit, there are unconfirmed reports that a few other banks are towing this

line, expectedly so.

[READ: After GTBank, Sterling Bank is restructuring into a holdings company]

Now, jargons aside, becoming a holding company basically allows these banks to officially do more things apart from banking; see my joke above.

But seriously, word on the street is that all the suite of services from fintech startups are the main targets for these banks, especially payments.

“GTBank is going to win [the payment space],” he said on stage, “and we’re going to win very easily,” the bank’s CEO Segun Agbaje recently bragged.

Maybe he’s right, and there will be a fintech bloodbath. Afterall, banks have numbers that fintech startups can only dream off.

Maybe he’s way off the mark and the nimble nature of startups will allow innovations and iterations that these banks will not be able to match.

Maybe there’s hope in collaboration. Most fintech companies either own banks, are affiliated in some way with others or just plain need them to survive. Either way, consolidations, acquisitions, acqui-hires and outright obliterations will happen in the Nigerian fintech space in the nearest future. 2021 will be an interesting year for fintech.

|

|

|

|

|

|

|

Investing in francophone Africa’s tech startup ecosystem.

The Francophone business law system in Africa is unified. But regardless of this unification, most business concepts that can be easily used in most countries in anglophone Africa cannot be implemented without certain key adjustments.

For the first version of our new TC Regulate

series, our guest contributor does justice to the topic.

Why is Facebook really coming to Nigeria? Four years after its CEO, Mark Zuckerberg landed in Lagos, the social media giant has announced a robust plan for Nigeria. Beyond the numerous new talent joining the H1 2021 office, here’s a deep dive that explains reasons beyond a surface story.

|

|

|

|

|

|

|

“The effects of COVID-19 have highlighted a number of aspects to both work & day-to-day life that require changing habits and a paradigm shift, as well as the need for

investment in a more robust infrastructure. We’ve seen the limitations of cash, anyone outside an urban hub, e.g. farmers, would have had challenges too.

So financial inclusion on its own couldn’t help. New ways of making payments are clearly essential – this must be inclusive even from a geographical perspective. COVID conditions have revealed that cash is financially exclusive under certain conditions. Going forward, we will need a new enabling environment that facilitates digital liquidity. This starts with digital identity. We need to know who people are. This will promote social inclusion that allows the government to access information about the makeup of Nigeria’s citizenship and provide equitable social services that will

promote even tax inclusion and financial inclusion. You can’t be financially included if there is nothing to pay into your account.“

– Uzoma Dozie, Founder and CEO, Sparkle.

Every week, we will ask our readers, stakeholders, and operators in Africa’s tech ecosystem what they think the new normal will look like, and will share their thoughts here. You can share yours with victor@bigcabal.com with ‘The Crystal Ball’ in the subject line.

|

|

|

|

|

|

|

New Normal

Hauwa (not real name) got her first job, a blue collar one, during the pandemic. She then needed to open a salary account. On a Monday afternoon, she went to the nearest bank to her home in Lagos Island around 12:15pm and didn’t return home until 7pm. The bigger problem was that she couldn’t open the salary account.

One thing that has become constant in banks across Lagos, Nigeria are queues. Although the queues are mostly a result of safety precautions being taken by banks, they are a reflection of the low adoption of the digital channels provided by banks. Hauwa returned one more time to the bank before she finally gave up opening a bank account.

|

|

|

|

|

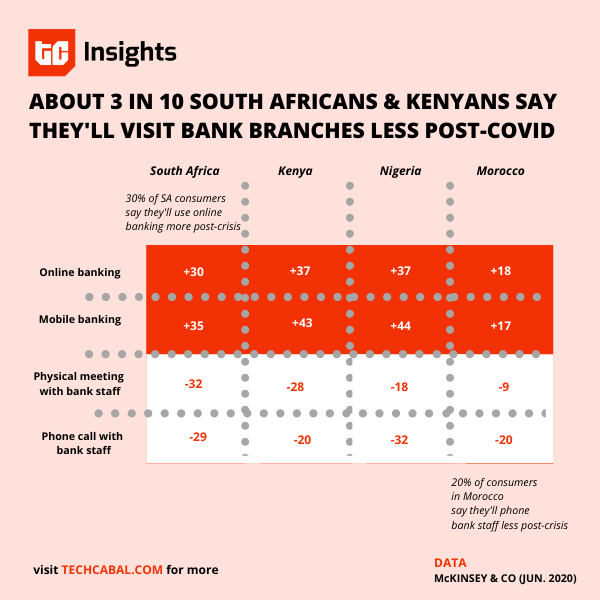

Banks in Nigeria and across Africa, have invested in digital channels over the last few years. And while they’ve seen some adoption among the more educated and internet-savvy population, the majority of the banked in many countries still prefer to walk into bank branches. If you’ve got a complaint, you are more likely to get it resolved if you walk into your bank.

Yet there’s growing evidence that customers actually prefer ease and convenience. At the start of the pandemic, customers relied largely on their bank’s digital channels due to mandatory lockdowns. And a McKinsey study that looked at the effect of the pandemic on banking in Africa learnt that customers in Nigeria, South Africa, Kenya and Morocco planned to use digital channels more often post-COVID.

It’s great news for banks but won’t mean much if they don’t invest in customer education, putting users at the center of their shiny new apps and making dispute resolution far easier. Digital could become the new normal for banking only if banks build with the customers in

mind.

If you are a founder in Africa, please fill our investor list here and let us know who gave you your first check. Get TechCabal’s

reports and send us your custom research requests here.

|

|

|

|

|

Best wishes for a great week

|

|

|

Stay safe and please observe all guidelines provided by health experts.

You can subscribe to our TC Daily Newsletter; the most comprehensive roundup of technology news on the continent, and have it delivered to your inbox every weekday at 7 am WAT.

Follow TechCabal on Twitter, Instagram, Facebook, and LinkedIn to stay updated on tech and innovation in Africa.

– Victor Ekwealor, Managing Editor, TechCabal

|

|

|

|

|

|

|

|

|

Sign up for The Next Wave

by TechCabal

|

|

|

|

|

|

|

|

|

|

|

Copyright © 2020 Big Cabal Media,

All rights reserved.

You are receiving this email because

you signed up on TechCabal.com

Our mailing address is:

Big Cabal Media

18, Nnobi Street, Animashaun, Surulere, Lagos

Surulere 100001

Nigeria

Add us to your address book

Want to change how you receive these emails? You can

|

|

|

|

|

|

|