|

|

|

|

|

|

NOVEMBER 8, 2020

This newsletter is a weekly in-depth analysis of tech and innovation in Africa that will serve as a post-pandemic guide. Subscribe here to get it directly in your inbox every Sunday at 3 pm WAT.

|

|

|

|

|

|

|

|

|

So much has happened in the last week, but that’s the pace 2020 has been on. Nothing surprising there.

Joe Biden is now the president-elect of the USA, and Kamala Harris is the first female, black, Asian, VP, ever. Plenty firsts, phew!

Back home, TechCabal hosted Paystack’s CEO, Shola Akinlade in a long refreshing conversation, the first since the $200 million exit to Stripe. ICYMI, here’s a YouTube link.

While Akinlade was talking about a range of topics from early days, to everything else fintech, WhatsApp was making a fintech move halfway across the world.

After more than 2 years of testing, the world’s biggest instant messaging platform announced its

payment service in India.

This got me thinking that WhatsApp pay would indeed be a game-changer in Africa, but there might be hurdles to adoptions and implementation.

Today, while answering the “what about Africa” question, I am going to revisit a 3-year-old prediction and make even more predictions, that you may or may not agree with.

But first, subscribe to this newsletter if it was

forwarded to you, and check out older editions from past weeks.

And oh, there’s still a pandemic, wear a mask, please.

|

|

|

|

|

|

|

Of crystal balls, and adoption wahala

In August 2017, I predicted that WhatsApp Pay would come into Nigeria, disrupt it and, in my own words,

“pose great competition to players in the industry“.

This assertion was based on available information to me at the time, and on a scale of wrong to right, it tilted more to the former; WhatsApp Pay did not come. Nigeria’s fintech industry trudged on to great heights.

The Indian, and Asian, markets are similar to most of Africa’s especially in terms of population size, and a lot of innovation models have been copied from India to the continent. Motorcycle hailing startups are the biggest example of this, and solutions from big tech companies like Facebook and Google are tested there before coming to Africa.

All these, in addition to the ever improving maturity levels of payments on the continent, are indicators that WhatsApp Pay will come here soon.

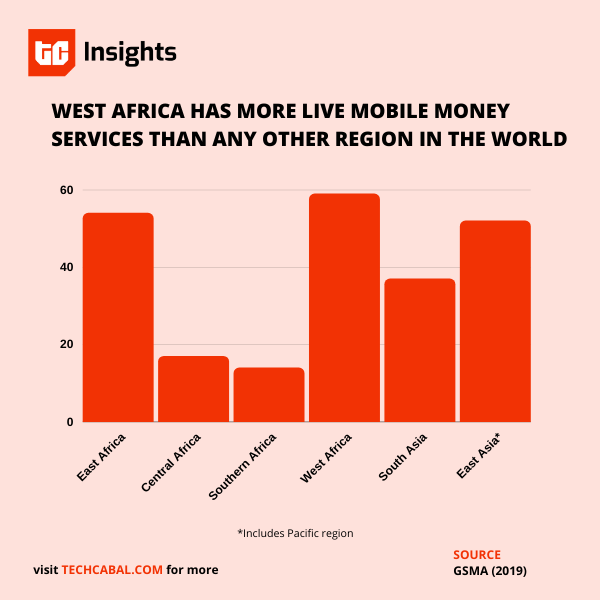

In 2019, Africa added 50 million mobile money accounts, with East Africa remaining number 1 in the world in terms of transaction volume and value;

“The region’s 102 million active accounts is the highest in any sub-region; its 17.1 billion transactions generated an unmatched $293.4 billion in value, a 24% increase from 2018.”

[READ: West Africa is Africa’s mobile money rising star]

|

|

|

|

|

While fintech infrastructure and payments are ramping up, smartphone adoption and broadband connectivity are still low.

Earlier in the year, thanks to the pandemic, smartphone factories were shut and these already low numbers most likely took a hit.

[READ: Could Africa run out of new smartphones in 2020?]

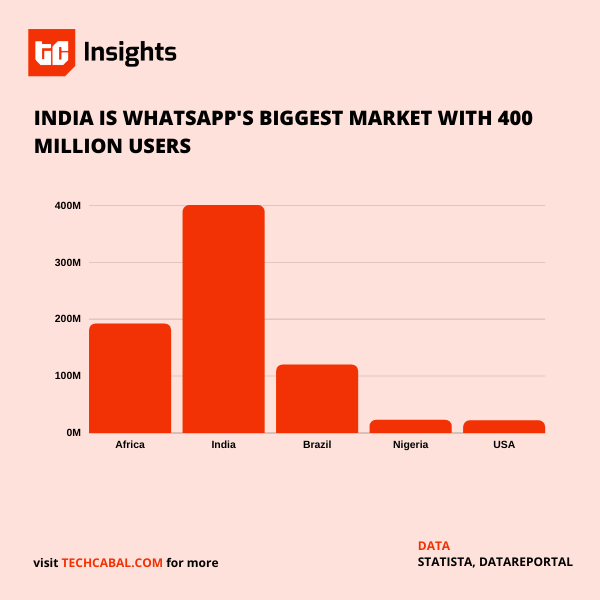

From a more holistic perspective, while Africa as a continent had 272 million internet users in 2019 and is projected to reach 475 million by 2025, India alone has 400 million WhatsApp users; the difference is stark.

|

|

|

|

|

Regulatory and infrastructural scythes

Apart from the smartphone and internet end of things, regulations are another serious concern.

Central banks and regulatory agencies in many African countries are historically anti-innovation and can sometimes enact rules that impede growth.

[READ: The Next Wave: Regulatory mixed bags]

Countries where mobile money already thrive; like Kenya in East Africa, Ghana in West Africa, and Zimbabwe in South Africa, may not prove too much of a regulatory hurdle as the government has been eased into payments regulations, but this won’t be the case everywhere, and Nigeria is a big example.

Over the years, the Central Bank of Nigeria (CBN) through its bank-led model has subtly frustrated telcos from actively participating in the payments ecosystem. This is largely anti-competitive and is aimed at protecting the sovereignty that commercial banks enjoy. And also preventing the repeat of the Kenyan situation where

even though Safaricom did not necessarily replace banks, they have incredible power over the market.

With its current scale of a hundreds of millions of users in the continent, asides from the clueless policy making around here, this fear of a monopoly will be rife.

When Brazil suspended WhatsApp Pay earlier in the year, the central bank said they want to:

“Preserve an adequate competitive environment in the mobile payments space and to ensure functioning of a payment system that’s interchangeable, fast, secure, transparent, open and cheap.”

This lack of context will be a major concern for regulators across the continent who still struggle to grasp, what has become, basic fintech operations.

Also, it doesn’t help that there is no unifying fintech infrastructure across the continent.

India’s Unified Payments Interface (UPI) pulls users’ information from across over 160 banks into one place. Africa has a more fragmented structure.

For example, Kenya is mobile payments first, while Nigeria is bank-led.

Now the question becomes, will the small numbers of users be worth the pains of navigating these fragmented infrastructural terrains across the continent?

From a long term perspective, yes.

Fintech in Africa has come a long way, too long for WhatsApp to edge out already existing players. If anything, there’ll be more synergy than competition across the board. A likely situation will see Interswitch as a Third Party Service Provider (TPSP) for WhatsApp Pay on the continent, integration with other banks and fintech companies like Paystack (Stripe) and Flutterwave.

“On the other hand,WhatsApp Payments may just be an

enabler for the fintech industry in Nigeria [Africa] if things are done right.

All things being equal, WhatsApp will need a gateway to facilitate these transactions and existing players in the industry are the only available gatekeepers. For existing players in the Nigerian fintech industry, enabling WhatsApp Payments may be the push they need to gallop to greater adoption rates.”

The aforementioned quote is the only part of that 3-year prediction that I believe will hold true.

|

|

|

|

|

|

|

Gokada will go on

It’s been 4 months since the brutal murder of its founder and former CEO Fahim Saleh, Gokada is forging ahead.

The Nigeria-based motorcycle hailing startup is now under new leadership and Nikhil Goel, Gokada’s COO and President tells TechCabal how they are making progress in leaps with Saleh’s vision.

An African loan marketplace. This week’s edition of The BackEnd series features Evolve Credit wanting to be an authoritative loan and financial products marketplace

for Africa, starting with Nigeria.

This story explains how they are working at user personalization and sector regulation in a largely unregulated industry.

|

|

|

|

|

|

|

“COVID-19 forced formal learning to migrate online for a privileged few and brought it to an abrupt halt for the vast majority of secondary learners, who have had to rely on analogue approaches such as TV and Radio. The sad truth is that for the vast majority, the new normal will remain the same.

We now have an opportunity to use technology to transform societal approaches to education. Investing in the digitisation of education and learning management platforms

presents a short-term opportunity for ed-tech investors and innovators. A medium-term opportunity exists in content development and teaching broadcast, and a long-term challenge remains in cracking the hardest problems of personal mastery, cognition and concept assimilation at scale.”

–

Tunji Adegbesan, founder and CEO, Gidi Mobile

Every week, we will ask our readers, stakeholders,

and operators in Africa’s tech ecosystem what they think the new normal will look like, and will share their thoughts here. You can share yours with victor@bigcabal.com with ‘The Crystal Ball’ in the subject line.

|

|

|

|

|

|

|

New Fintech

“Payments have been figured out. The next step is how can we enable other companies with data. That’s why you see companies like Okra and Mono coming up,” Abdulhamid Hassan, the co-founder of API fintech startup, Mono recently told TechPoint.

His company is one of the three new, API fintech startups in Nigeria within the last year. Their API helps companies access banking information of customers to complete transactions in a seamless manner.

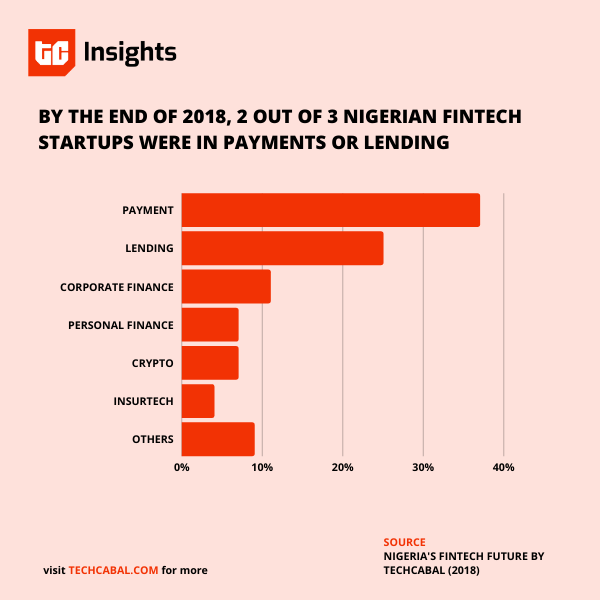

By the end of 2018, at least

2 in 3 fintech startups in Nigeria were either in payment or lending according to data collected by TechCabal.

|

|

|

|

|

Payments startups led the pack with about 37% of fintech startups being in the sub-sector.

But 2018 was the year that saw an explosion of crypto startups. Although Quidax and Buycoins were founded in 2017, they didn’t really take off until 2018. In 2017, personal finance startups helping consumers save (e.g. PiggyVest) and track expenses (e.g. Reach) became active on the scene.

Every year in the last four years has seen one fintech trend or the other become prominent in Nigeria.

2020, it appears, is the year of API fintech. A year ago it was investment-related

fintech companies specifically those focused on foreign investment opportunities.

Fintech trends are not an unusual phenomenon although they might be interesting to watch. There are several theories as to how these trends happen. As startups begin to emerge in a certain sub-sector and investment begins to flow there, more entrepreneurs attempt to solve problems in that sub-sector.

Another theory is that problems evolve and industries advance. For example, it would have been impossible to build many of the Nigerian

fintech startups that exist without first solving the payments problem. API fintech startups possibly emerged as existing startups began to face problems with accessing and verifying customer data.

One other theory is perfectly described by Ope Adeoye, founder of One Pipe, another API fintech, as a local expression of trends from advanced markets. This theory says major global events like the acquisition of Plaid by Visa in January 2020 drive trends in local markets like Nigeria.

The key question with trends especially the expression theory is whether there’s product-market fit and a large enough market for a service.

If you are a founder in Africa, please fill our investor list here and let us know who gave you your first check. Get TechCabal’s reports and send us your custom research requests here.

|

|

|

|

|

|

|

|

|

Best wishes for a great week

|

|

|

Stay safe and please observe all guidelines provided by health experts.

You can subscribe to our TC Daily Newsletter; the most comprehensive roundup of technology news on the continent, and have it delivered to your inbox every weekday at 7 am WAT.

Follow TechCabal on Twitter, Instagram, Facebook, and LinkedIn to stay updated on tech and innovation in Africa.

– Victor Ekwealor, Managing Editor, TechCabal

|

|

|

|

|

|

|

|

|

Sign up for The Next Wave

by TechCabal

|

|

|

|

|

|

|

|

|

|

|

Copyright © 2020 Big Cabal Media,

All rights reserved.

You are receiving this email because

you signed up on TechCabal.com

Our mailing address is:

Big Cabal Media

18, Nnobi Street, Animashaun, Surulere, Lagos

Surulere 100001

Nigeria

Add us to your address book

Want to change how you receive these emails? You can

|

|

|

|

|

|

|